Summary

As Northeast Asia, Europe and North America move into spring, the markets could cool as temperatures rise. Pressure on hub prices is expected to increase over the coming weeks.

Forecast highlights

- Northeast Asian spot LNG prices for April delivery have fallen to around $4-4.5/MMBtu and are expected to come under further pressure as the spring gets underway. There is scope for demand-side support if the summer proves to be hotter than average, as initial forecasts for Japan indicate.

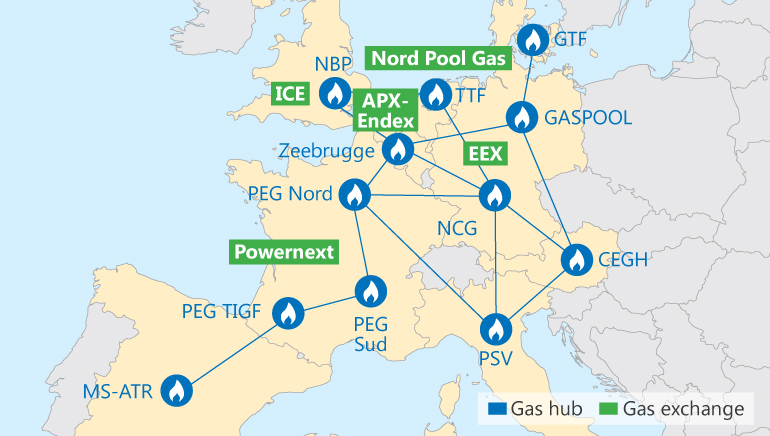

- European month-ahead prices remain below 30 p/th and are likely to decline further over the coming weeks. Strong flows from Norway and Russia, in addition to LNG imports, will help outweigh the drops in indigenous European supply caused by declines in Dutch output.

- The Henry Hub front-month futures price may struggle to move above $2/MMBtu during the spring. Forecasts for mild weather and the onset of the 2016 gas-injection season are both bearish factors for the price.

- The outlook for regional spot gas prices in the US and Canada over the coming months is bearish as the gas injection season begins in April. This will also reduce price volatility at key pricing points such as the Transco Z6 in New York.

- There is little sign that LNG demand in Latin America will increase substantially during the southern hemisphere autumn. This will add further pressure to the region’s spot LNG price. The price is unlikely to go over $10/MMBtu even during the peak winter demand period.

- Turkey will continue to take advantage of low LNG prices and is expected to procure additional volumes on the spot market in the coming months. Separately, prospects for a 10-15% discount on pipeline gas from Iran may boost the attractiveness of Iranian gas in Turkey during summer.

- The Brent crude price rose above $40/bbl in March after averaging around $33.5/bbl in February. However, further gains will be limited as bearish fundamentals will continue to put pressure on prices.