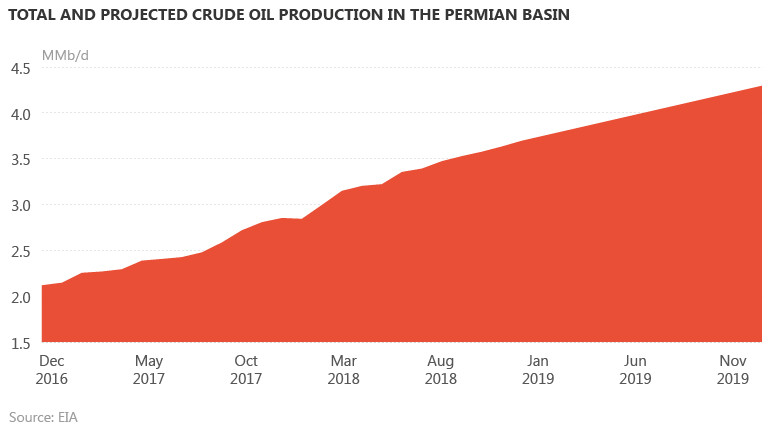

The Permian basin in the United States is the fastest-growing source of oil production in the world. Output from the Permian, located in western Texas and southeastern New Mexico, is projected to rise by 600,000 barrels per day year on year in 2019, according to the US Energy Information Administration. With production expected to reach 3.7 million b/d (MMb/d) in 2018, this means output is expected to be about 4.3 MMb/d by the end of 2019, as shown in the chart below.

Flood of associated natural gas

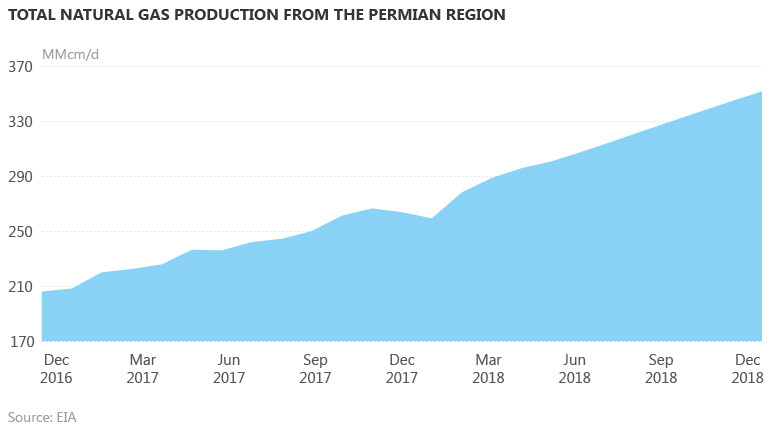

The Permian is not only seeing huge growth in oil production, but also producing a veritable flood of associated gas, as shown in the chart below.

Permian producers are not drilling for this gas on purpose; they are drilling for oil. This flood of gas is happening despite the lack of a local market for additional volumes in the region.

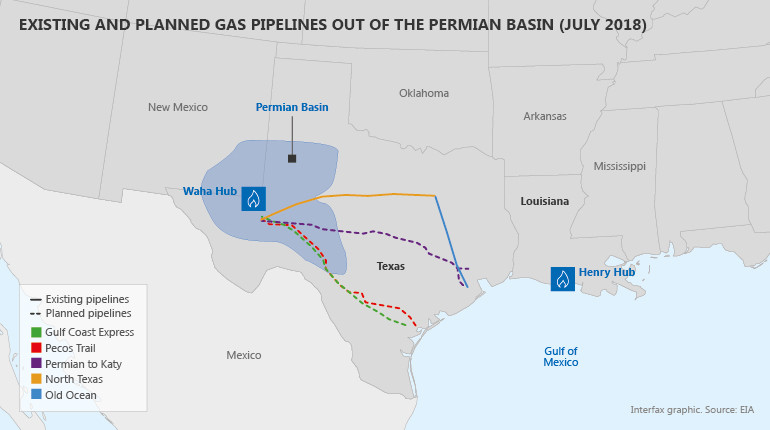

All the additional gas has to be transported by pipeline away from the Permian fields or flared if the pipelines are full. Much of the incremental gas is delivered to the Texas and Louisiana Gulf Coast region. The map shows existing and planned gas pipelines from the Permian. As shown, all of these pipelines are aimed at the Gulf Coast.

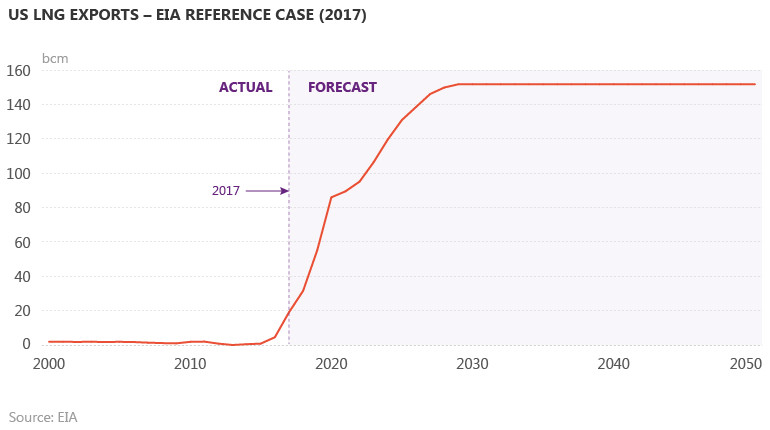

The growth in Permian gas production is expected to continue and to overwhelm US markets. Some of it will be exported by pipeline to Mexico. From January to May 2018, west Texas pipeline exports to Mexico averaged only 14 million cubic meters per day (MMcm/d). Eventually, all of the excess Permian volumes are expected to be exported as LNG from new liquefaction plants on the Gulf Coast in Texas and Louisiana. The chart below shows the US is expected to export 425 MMcm/d of LNG by the late 2020s. Clearly, the marginal molecules of Permian gas will be exported as LNG from the US Gulf Coast.

US Gulf LNG indexed to Henry Hub, not oil

The LNG business was conceived and built on crude oil price indexation for the pricing of firm LNG deliveries to Japan, South Korea and Taiwan (JKT). In its early days, LNG was usually used to displace oil or oil products used to fuel power stations. Almost all legacy LNG suppliers – including Indonesia, Malaysia, Qatar, Australia and the US from Alaska – used oil-indexed price formulas for their LNG and drew gas feedstock from specific producing fields. Furthermore, the LNG contracts were of the long-term, firm ‘take or pay’ variety, with little or no volume flexibility.

Pricing formulas in this legacy LNG business model would typically be similar to the following:

- LNG delivered price to JKT in $/MMBtu = Brent crude price in $/bbl x 14.4% + $0.50/MMBtu.

- Thus, if Brent oil price is $80/bbl, the JKT delivered LNG price is about $12/MMBtu.

However, starting in 2016 a new breed of US LNG exporter was born. Instead of selling LNG itself, this new breed – characterised by Cheniere Energy – sells firm liquefaction services, in essence. Feedstock is supplied from the pipeline grid as opposed to specific producing fields. Even though in its case Cheniere buys the gas, its customers ultimately bear the gas and LNG price risks. Cheniere’s LNG plants liquefy the gas and load it onto ships for its customers to transport as they see fit. The long term, firm customers pay a pre-set, take-or-pay toll for the liquefaction services. Typical tolls are in the range of $3/MMBtu. Assuming US gas prices are about $3/MMBtu and shipping costs from Louisiana to JKT are about $2/MMBtu, then the LNG tolling customers are paying $8/MMBtu for LNG delivered to JKT that is worth $12/MMBtu.

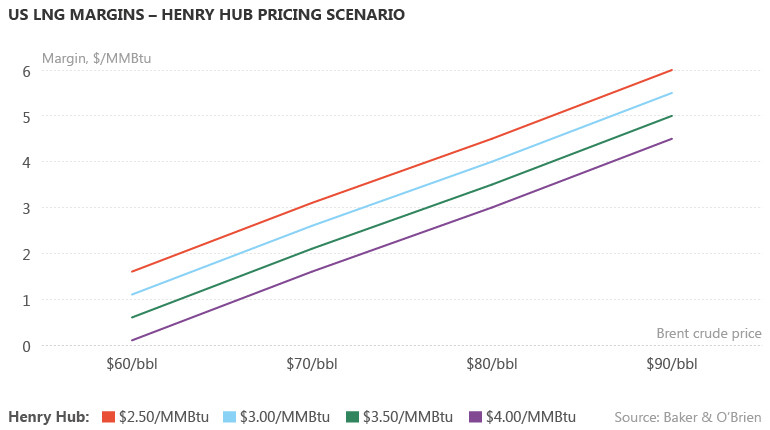

That is a $4/MMBtu margin over cost for the new breed of US LNG exporter under current and assumed pricing for gas, oil and LNG. The chart below presents illustrative margins depending on prices for Brent crude and Henry Hub gas.

This development raises a number of questions. For example, many Asian LNG buyers have complained for years about their oil-indexed, long-term contract prices. What will they do now? Should legacy LNG suppliers expect to re-open price negotiations with their buyers? And what are the implications for other factors such as destination restrictions and contract term length?

Robert Beck is a Consultant with Baker & O’Brien. Robert can be contacted at [email protected].

Baker & O’Brien Incorporated is a leading international oil and gas consultancy serving a wide variety of clients with interests in the oil, gas, chemicals, and related industries: http://www.bakerobrien.com

- Liked this article?

- Stay informed with exclusive, accurate and up-to-date energy news, analysis and intelligence. Sign up for 7-day trial access to more premium content. It's free!

- Get a free trial